With enhanced Affordable Care Act (ACA) subsidies set to expire on December 31, the Senate is turning its attention to health care this week, setting up a high-stakes test of competing visions for coverage, costs, and the federal role in the individual market. The political calculus is sharp: millions of marketplace enrollees could face sizable premium hikes in 2026 if no deal emerges, while both parties weigh how any vote will resonate with independents heading into the new year.

ACA subsidies extension: the immediate fight

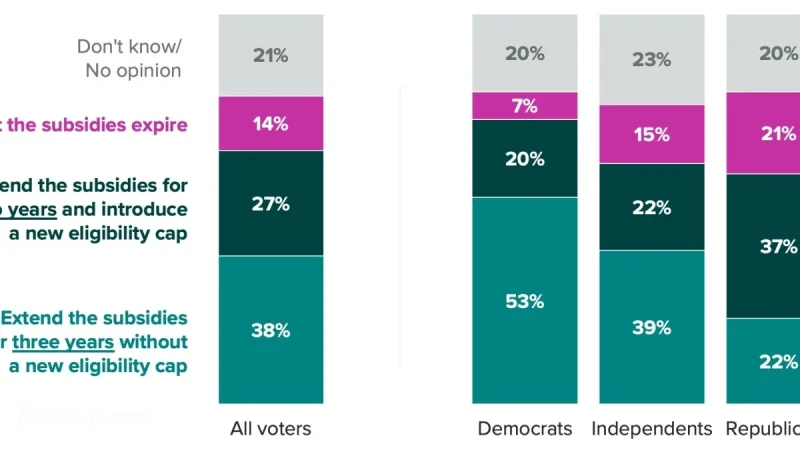

Democrats are rallying behind a three-year extension of the pandemic-era enhancements that cap benchmark silver plan premiums at 8.5% of income and expand eligibility above 400% of the federal poverty level. The pitch is simple and urgent: lock in affordability through 2028 to avoid a sharp “subsidy cliff” when 2026 premiums take effect.

Budget hawks counter that a multi-year extension would add meaningfully to the deficit, pressing lawmakers to justify the trade-offs or pair an extension with offsets. Even so, the core policy question remains near-term affordability vs. long-term cost control—an argument that has repeatedly stalled broader reform while the clock keeps ticking toward year-end.

Republicans’ health care plan: division over direction, not goals

Republicans agree on principles—lower costs, more choice, less red tape—but remain split over the how:

-

Targeted subsidies and phase-outs: Some propose re-tightening eligibility above 400% of poverty and requiring all households to contribute at least a token premium, even at low incomes, to avoid zero-dollar plans.

-

Plan neutrality and HSAs: Another bloc wants subsidies that don’t steer consumers toward richer silver plans; instead, aid would be more neutral across bronze/silver with greater use of health savings accounts to promote price sensitivity.

-

Short extension with reforms: A pragmatic camp is open to a shorter extension (one to two years) paired with technical changes—like adjusted income calculations or anti-churn safeguards—to buy time for a broader package.

The White House has floated the contours of a temporary extension with eligibility adjustments, but internal GOP differences over scope and pay-fors have kept a unified plan from advancing. The result: Democrats can force a vote on a clean extension, while Republicans debate whether to present a fully formed alternative now or fold the issue into the next government funding deadline expected in late January.

What happens if ACA subsidies lapse?

If the enhancements end on December 31, consumers would feel the impact when 2026 rates hit:

-

Premium spikes: Analyses indicate sizable increases—often hundreds of dollars more per month for older, middle-income buyers—because the 8.5% income cap would end and the pre-2021 subsidy formula would return.

-

Coverage risk: Enrollment could fall as price-sensitive shoppers exit, especially in rural counties where marketplace plans are already thin and premiums relatively high.

Related News

-

Carrier responses: Insurers may reprice or narrow networks further for 2026 to reflect a sicker risk pool if healthier enrollees leave.

Key numbers shaping the debate

-

57% approval of the ACA: Public support has edged to a recent high, driven by independents—raising the political cost of inaction for both parties.

-

Hundreds of billions over a decade: Permanent extension scenarios add significantly to federal deficits without offsets; multi-year extensions still carry large price tags.

-

Disparate state impacts: States with older enrollees and higher benchmark premiums (often rural or low-competition markets) would see the steepest net premium jumps if enhancements sunset.

Timelines, votes, and what to watch next

-

This week: Senate floor time is expected on a three-year extension. Even if the measure fails procedurally, it will frame negotiations and put senators on record.

-

Open Enrollment (now through mid-January in most states): Consumers choose 2025 coverage under current rules. The real affordability shock comes with 2026 pricing if Congress doesn’t act in time.

-

Late January deadline: Broader negotiations could resurface around the next funding milestone, a likely vehicle for a shorter extension or a modest reform package.

How competing proposals compare

| Scenario | Affordability (near-term) | Federal cost | Market stability | Politics |

|---|---|---|---|---|

| 3-year extension | High—keeps 8.5% cap, broad eligibility | High, without offsets | Strong—avoids 2026 “cliff” | Clear vote; energizes base and independents favoring ACA |

| No extension | Low—premiums jump in 2026 for many | Lower federal spending | Weaker—risk of enrollment drop, adverse selection | Politically risky in swing areas |

| Short extension + reforms | Moderate—softens cliff, adds conditions | Moderate | Moderate—buys time, nudges plan mix | Could draw bipartisan support if offsets align |

| Neutral subsidies + HSA push | Varies—more help for bronze buyers, less tilt to silver | Potentially lower per-enrollee | Mixed—depends on consumer response and network adequacy | Appeals to cost-control voters; details matter |

What consumers should do now

-

Complete 2025 enrollment before deadlines; current enhancements remain in place next year.

-

Compare plan metal tiers carefully; zero- or low-premium bronze plans may have higher deductibles, while silver still brings cost-sharing reductions for eligible enrollees.

-

Watch Washington’s calendar: The December 31 subsidy deadline and late-January negotiations are the critical markers for 2026 affordability.

ACA subsidies and Republicans’ health care plan

The fight isn’t about whether to lower premiums—it’s about how, for how long, and who pays. Democrats want a straight multi-year extension to preserve affordability and prevent a 2026 shock. Republicans are divided between short-term extensions with guardrails and broader structural changes that shift more decisions—and some costs—to consumers. With the Senate spotlight now fixed on the issue and another fiscal deadline looming, a narrow deal is possible. The price of failure, measured in 2026 premium notices, would be immediate and highly visible.