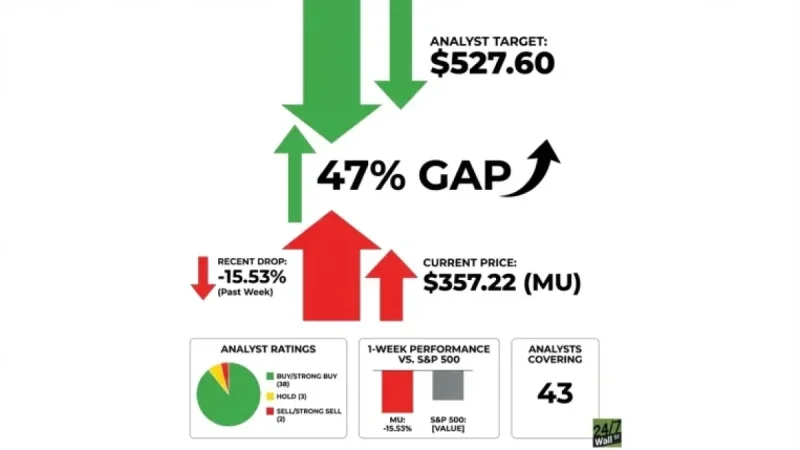

The recent decline in Micron Technology’s stock has raised concerns and attention on Wall Street. Currently, Micron’s shares are priced at $357.22, while analysts maintain a higher target of $527.60, indicating a potential upside of about 47%. This discrepancy requires a thorough examination of the situation to determine if it signals an opportunity or warns of underlying issues.

Understanding Micron’s Market Position

Micron is the sole U.S.-based producer of DRAM and a major supplier of NAND memory chips, making it crucial for the growing AI infrastructure. CEO Sanjay Mehrotra has emphasized Micron’s role in the semiconductor industry, particularly in enabling advancements in artificial intelligence. Over the past year, Micron’s stock has surged by an impressive 291.9% before facing recent setbacks.

The Impact of Google’s TurboQuant Algorithm

A significant factor contributing to Micron’s recent stock decline was announced on March 24, when Google introduced its TurboQuant algorithm. This new technology drastically reduces memory requirements for AI tasks, resulting in a sector-wide sell-off in memory stocks. On that same day, shares of Lam Research (NASDAQ: LRCX) plummeted by 9.4%, while Micron experienced a 15.5% drop in just one week and a 13.4% decline over the past month.

Investors are now reassessing the potential demand for memory driven by AI, fearing that the supercycle that fueled Micron’s revenue growth might be less robust than anticipated. Importantly, this sell-off appears to affect the entire memory sector, rather than being specific to Micron alone.

Analyst Confidence in Micron

Despite recent trends, Wall Street remains optimistic about Micron. Out of 43 analysts monitoring the company, 38 rate it as a Buy or Strong Buy. Only three rate it as Hold and two as Sell. J.P. Morgan, for example, has set a price target of $550, based on solid fundamentals that are unaffected by TurboQuant.

Micron’s revenue growth has been notable, rising from $8.053 billion in Q2 FY2025 to $23.86 billion in Q2 FY2026, with expectations for Q3 FY2026 reaching $33.5 billion. The gross margin also improved significantly, from 36.8% to 56.0%, and is projected to hit 67.0% next quarter. Mehrotra confirmed that the entirety of the calendar 2026 HBM supply is already booked for sale.

Key Financial Metrics

| Metric | Value |

|---|---|

| Current Price | $357.22 |

| Analyst Consensus Target | $527.60 |

| Implied Upside | ~47% |

| Analysts Covering | 43 |

| Buy/Strong Buy Ratings | 38 |

| 1-Week Performance | -15.5% |

| YTD Performance | +25.2% |

The Risks Involved

While the fundamentals support a bullish outlook, potential risks remain. The pivotal concern is that TurboQuant may indicate a structural shift in memory demand. If true, it could render current revenue projections and analyst targets overly optimistic. Micron’s heavy capital expenditure plan of approximately $25 billion in fiscal 2026 heightens the implications of a demand slowdown.

Additionally, recent insider selling adds a slight cautionary element. Yet, many analysts view the recent stock declines as an overreaction. The disparity between Micron’s current market price and the company’s comprehensive performance suggests that there may be more opportunity than risk in the long run.