Commonwealth Bank says customers can now join in under one minute using cba share price-adjacent digital trust tools that tap an ePassport against a phone. The change is simple on the surface: one document, one scan, one selfie. But it also reveals a deeper shift in how Australia’s largest banks are treating identity, fraud prevention, and the speed of digital onboarding.

What is the central question behind this passport change?

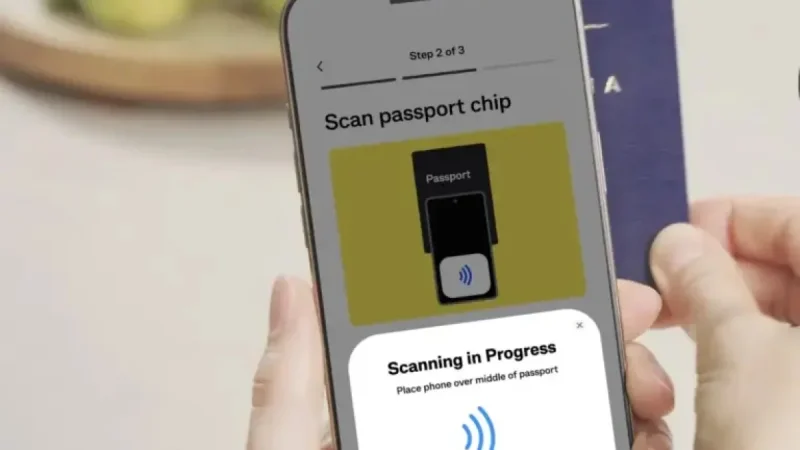

The central question is not whether the process is fast. It clearly is. The more important question is what this fast lane means for customer verification in a banking system where identity is becoming both a convenience feature and a security battleground. Commonwealth Bank says its new system uses near-field communication technology to read the chip embedded in Australian ePassports, then pre-populates the application form and matches the passport image with a customer selfie.

Verified fact: the bank says more than 2, 700 customers had used the feature since its launch at the end of January. Verified fact: customers no longer need to provide two separate documents in the digital application flow. Verified fact: the bank says the biometric information is read from the ePassport chip and used to confirm the customer’s identity. The larger implication is that onboarding is being redesigned around a single trusted document and a live face match, rather than a multi-document paper trail.

How does the new system change the onboarding process?

Commonwealth Bank general manager of customer identity and digital security Sascha Thiel said the system is intended to be “a really simple, safe, secure way” to prove identity online and that customers could join the bank “in under one minute. ” That is the headline promise, and the bank presents it as a practical upgrade for both speed and security.

Before the change, digital applicants needed two document types, such as a passport and a driver’s licence. Now, the bank says the app can read the cryptographically encrypted data from the ePassport, populate the form, and unlock the government-issued biometric stored in the chip. The customer then takes a selfie, and the two are matched to confirm identity.

In plain terms, the new process reduces friction. In investigative terms, it also consolidates trust into a tightly controlled digital interaction. That matters because the system is not just about convenience; it is also meant to counter fraud patterns that exploit weak or fragmented identity checks. In this case, the bank’s own framing places the technology at the intersection of onboarding efficiency and fraud resistance.

Who benefits from the shift, and who is being addressed?

The immediate beneficiaries are customers who want faster account opening, and the bank itself, which can streamline onboarding and reduce manual checks. Commonwealth Bank says the app feature is available on iOS and Android, and that the flows are designed by the bank rather than handed to a third-party provider. The bank also says the biometric is not retained or stored, and that the image is used only to unlock and verify the government-issued photograph.

Sascha Thiel said the move should also help combat scams and “synthetic identity fraud, ” which he described as criminals combining real and fake information to create false identities. That is the most telling justification in the story. The bank is not only selling speed; it is arguing that speed can coexist with stronger protection when identity proofing is pushed deeper into encrypted document verification.

For now, the feature is available to Australian customers, with an expansion planned for migrants moving to the country and overseas students. That future rollout suggests the bank sees the process as more than a niche convenience. It is being positioned as a scalable onboarding model for people who may need a clearer digital route into the banking system.

What does this say about the wider banking race?

Verified fact: other banks already require selfie verification in online account opening. Verified fact: one major lender introduced the requirement for select products in September, and another uses selfie checks for account setup, PIN resets, and payment limit increases. Verified fact: one bank said its process reduced onboarding time by around 50 per cent. Those details show that Commonwealth Bank is entering a broader race to compress onboarding time without loosening controls.

Informed analysis: the competitive pressure is now moving from “can a customer open an account digitally?” to “how few steps can be used while still satisfying identity and anti-money-laundering requirements?” Commonwealth Bank says its system is compliant with Australian privacy legislation and banking regulations for know your customer and anti-money laundering requirements. That compliance claim is important because it places the speed promise inside a regulatory frame rather than outside it.

There is also a strategic signal in the bank’s claim that it is the first in Australia with an NFC-based customer onboarding system. If that holds, the value is not only operational. It also gives the bank an early position in a model that may become standard as ePassports and mobile verification become more tightly linked.

What should the public take from cba share price and this new identity model?

The public takeaway is straightforward: the banking system is moving toward a future where trust is built into the phone itself, using encrypted passport chips, live selfies, and automated matching. That may reduce friction and make onboarding faster, but it also concentrates enormous responsibility inside a few digital checks. If those checks work well, they can make fraud harder. If they fail, the consequences are immediate.

For Commonwealth Bank, the passport change is more than a product update. It is a statement about where customer identity is heading and how quickly banking can be transformed when convenience and security are engineered together. In that sense, cba share price is not just a market phrase here; it sits beside a deeper question about whether the bank’s digital promise can keep pace with the risks it is trying to contain.