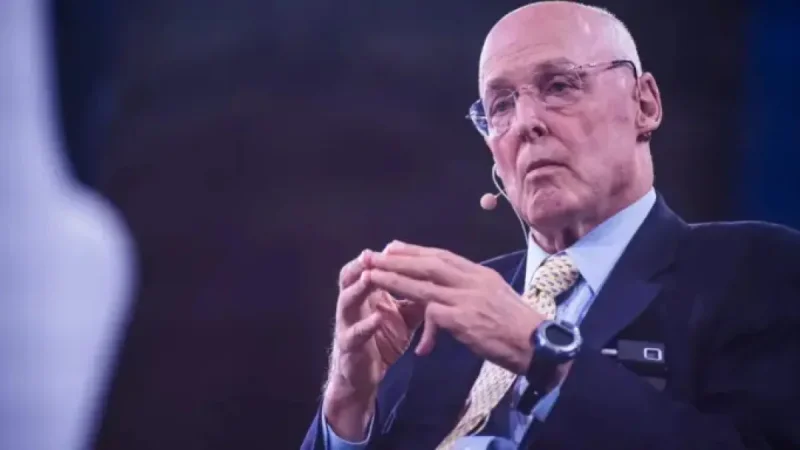

The phrase united states treasury security has moved from background market language into a warning sign. Henry Paulson, the former Treasury secretary, says the U. S. should have an emergency “break-the-glass” plan ready if long-running debt stress starts to weaken demand for government borrowing.

What Happens When Confidence Becomes the Story?

The immediate issue is not a sudden failure, but a slow erosion of confidence. The U. S. debt load has climbed to $39 trillion, and budget experts have warned that such borrowing may force harder choices about what the government can spend on. In that environment, the Treasury market remains central because it helps finance the government and shapes borrowing costs across the economy.

Paulson’s warning is directed at the possibility that demand for government debt could eventually fall sharply. He described that as “dangerous, ” especially if foreign interest declines and prices weaken at the same time. A United States Treasury Security is treated as a foundation of the global financial system, but the context around it is changing.

What If the Treasury Market Stops Absorbing Risk?

The Treasury market is the largest bond market in the world and has long been treated as a haven during periods of stress. That status supports the dollar’s role as the world’s reserve currency and gives the U. S. room to finance deficits. But the current debt trajectory is testing that reliability.

- Higher debt can push investors to demand higher yields.

- Higher yields can lift interest rates across borrowing categories.

- Rising rates can make deficits harder to resolve.

- If private demand weakens enough, the Federal Reserve could become a buyer of last resort.

That final step is part of what Paulson wants policymakers to avoid. He said an emergency plan should be short-term, targeted, and already prepared before pressure reaches that point. The Committee for a Responsible Federal Budget, a nonpartisan think tank, has also advocated for a similar approach, proposing a way for the government to navigate a stressed budget during the next downturn.

What If Policymakers Prepare Before the Wall?

The most likely near-term path is not a collapse, but continued strain. Paulson said the timing is hard to predict because it depends on the debt trajectory and the general economy. That uncertainty is exactly why he argues for preparation now rather than improvisation later.

Best case: lawmakers and officials agree on a narrow contingency plan that steadies expectations before stress intensifies. Most likely: debate continues, debt concerns remain elevated, and markets keep watching the balance between financing needs and investor confidence. Most challenging: demand weakens further, the Federal Reserve is pulled in as a backstop, and confidence erodes faster than policymakers can respond.

For now, the message is less about panic than about readiness. A United States Treasury Security still sits at the center of the system, but Paulson’s comments underline a deeper reality: the asset that anchors global finance depends on the belief that the U. S. can keep financing itself without reaching a breaking point. The reader should understand that the risk is not only about debt levels, but about how long confidence can hold under pressure. The practical move for policymakers is to build a response before the next stress test arrives, because once the wall is reached, the room for error shrinks quickly. united states treasury security

The broader lesson is that Treasuries remain powerful, but not invulnerable. Markets can tolerate strain for a long time; they are less forgiving when strain becomes habit. The question now is whether the U. S. treats that warning as a signal to prepare, or waits until the market forces the issue. united states treasury security